Calculation of advance payments. How to calculate advance payments for property taxes

Sometimes even experienced accountants have questions about how to calculate advance payments for income tax. Let's analyze some of them. The procedure for calculating and paying income tax and advance payments on it is established by Art. 286 and 287 of the Tax Code of the Russian Federation.

In accordance with paragraph 1 of Art. 55 and paragraph 1 of Art. 285 of the Tax Code of the Russian Federation, the amount of income tax is paid based on the results of the calendar year. The general formula for calculating tax looks like this (clause 1 of Article 286 of the Tax Code of the Russian Federation):

NP = NB x C,

where NP is the income tax calculated for the tax period;

NB - tax base for the tax period;

C is the tax rate.

During the tax period (calendar year), organizations must calculate quarterly advance payments, which can be paid in three ways:

organizations whose revenue for the previous four quarters did not exceed an average of 10 million rubles. for each quarter, pay advance payments based on the results of the first quarter, half a year and 9 months without paying monthly advance payments;

at the end of each month, based on the actual profit received, advance payments are made to organizations that have expressed a desire to pay advance payments in this way and notified the tax office about this no later than December 31 of the year after which the monthly procedure for paying advance payments will be applied (this tax payment procedure beneficial if the organization’s activities are unstable, subject to the influence of seasonal and other factors, and a very significant income in one month can be followed by “failure” in others);

based on the results of the first quarter, half a year and 9 months, as well as advance payments for each month of the quarter are paid by all other organizations.

According to paragraph 1 of Art. 289 of the Tax Code of the Russian Federation, the calculation of the quarterly advance payment is made in the income tax return, which must be submitted to the tax office after the expiration of the corresponding reporting period. The form of the income tax return and the procedure for filling it out were approved by order of the Federal Tax Service of Russia dated March 22, 2012 No. ММВ-7-3/174@.

The procedure for calculating average income

In accordance with paragraph 3 of Art. 286 of the Tax Code of the Russian Federation, the revenue limit is 10 million rubles. used to determine whether an organization is obligated to make monthly advance payments in the current quarter. Therefore, based on the results of each past quarter, the organization must calculate the average amount of income from sales for the previous four quarters and compare it with the established limit. Only income from the sale of goods (work, services) and property rights, determined in accordance with Art. 249 of the Tax Code of the Russian Federation (non-operating income and income listed in Article 251 of the Tax Code of the Russian Federation are not taken into account). Sales proceeds are calculated excluding VAT and excise taxes.The date of inclusion of proceeds from sales in the income for which the average value is calculated is determined depending on the chosen method of recognition of income and expenses (cash method or accrual method).

The average amount of income from sales for the previous four quarters is calculated as follows: income from sales for each of the previous four quarters is summed up, after which the resulting amount is divided by four (arithmetic average). In this case, the calculation takes into account data for four consecutive quarters.

If the average sales revenue exceeds 10 million rubles, then from the next quarter the organization must pay monthly advance payments. At the end of the quarter, the calculation is made again.

EXAMPLE 1

The Cascade organization determines income and expenses for tax purposes using the accrual method.

Revenue for the previous year was:

in the first quarter - 8 million rubles;

in the second quarter - 11 million rubles;

in the third quarter - 10 million rubles;

in the fourth quarter - 13 million rubles.

In the current tax period, revenue indicators were:

in the first quarter - 4 million rubles;

in the second quarter - 20 million rubles.

Let us determine whether the organization is obliged to make monthly advance payments during the 1st, 2nd and 3rd quarters of the current tax period. To do this, it is necessary to calculate the average sales income for the previous four quarters.

I quarter

The value is determined based on the total amount of income received in the I-IV quarters of the previous year and is:

(8 million rubles + 11 million rubles + 10 million rubles + 13 million rubles): 4 = 10.5 million rubles.

The average sales income for the previous four quarters exceeds 10 million rubles. (10.5 million rubles > 10 million rubles). Consequently, in the first quarter the organization must pay monthly advance payments.

II quarter

The average amount of income from sales is calculated based on the total amount of income received in the 2nd-4th quarters of the previous year and the 1st quarter of the current tax period, and is:

(11 million rubles + 10 million rubles + 13 million rubles + 4 million rubles): 4 = 9.5 million rubles.

Since the amount received does not exceed 10 million rubles, during the second quarter the organization may not pay monthly advance payments.

III quarter

The average amount of income from sales is calculated based on the total amount of income received for the III-IV quarters of the previous year and the I-II quarters of the current tax period, and is equal to:

(10 million rubles + 13 million rubles + 4 million rubles + 20 million rubles): 4 = 11.75 million rubles.

The average income exceeds 10 million rubles. (11.7 million rubles > 10 million rubles), therefore the organization is obliged to pay monthly advance payments in the third quarter.

Procedure for calculating quarterly advance payments

The amount of the quarterly advance payment at the end of the reporting period is determined based on the actual profit, calculated on an accrual basis from the beginning of the tax period to the end of the reporting period (quarter, half-year, nine months), taking into account previously paid amounts of advance payments.In accordance with paragraph 2, clause 2, art. 286 of the Tax Code of the Russian Federation, the amount of the quarterly advance payment is equal to:

AK reporting = NB x C,

where reporting AC is the quarterly advance payment;

NB - tax base of the reporting period, calculated on an accrual basis from the beginning of the year to the end of the reporting period;

AK for additional payment = AK reporting - AK previous,

where AK for additional payment is the amount of the quarterly advance payment subject to payment (addition) to the budget at the end of the reporting period;

AK previous - the amount of the quarterly advance payment paid based on the results of the previous reporting period (in the current tax period).

EXAMPLE 2

The Cascade organization does not pay monthly advance payments. The tax base for income tax in the current year was based on the following results:

I quarter - 300,000 rubles;

in the first half of the year there was a loss of 100,000 rubles;

9 months - 600,000 rub.

The income tax rate is 20% (Clause 1, Article 284 of the Tax Code of the Russian Federation).

Let's calculate the amount of quarterly advance payments and determine the amount to be paid to the budget for each reporting period (Q1, half-year, 9 months). Let's look at the procedure for filling out a tax return.

1. The quarterly advance payment based on the results of the first quarter will be:

300,000 rub. x 20% = 60,000 rub.

The declaration for the first quarter must reflect the following indicators:

on line 180 of sheet 02 - the total amount of the quarterly advance payment based on the results of the first quarter - 60,000 rubles;

on lines 190, 200 of sheet 02 - the amount of the quarterly advance payment to be credited to the federal budget and the budget of the constituent entity of the Russian Federation - 6,000 rubles. and 54,000 rub. respectively.

Since the organization does not pay monthly advance payments, it must transfer the amount of the calculated advance payment for the first quarter (60,000 rubles) to the budget no later than April 28.

2. Let's calculate the quarterly advance payment for the six months. Since at the end of the six months a loss was received in the amount of 100,000 rubles, the tax base is recognized as zero (clause 8 of Article 274 of the Tax Code of the Russian Federation).

Accordingly, the calculated quarterly advance payment and the amount subject to payment (addition) to the budget at the end of the six months will also be equal to zero. In this case, the amount of the quarterly advance payment calculated and paid based on the results of the first quarter is subject to reduction and is recognized as an overpayment of tax.

The tax return for the half-year reflects the quarterly advance payment based on the results of the half-year as follows:

put dashes on lines 180, 190, 200 of sheet 02;

on lines 210, 220, 230 of sheet 02 - amounts 60,000 rub., 6,000 rub. and 54,000 rub. respectively;

on lines 270 and 271 of sheet 02 - dashes;

on lines 280 and 281 of sheet 02 - amounts of 6,000 and 54,000 rubles. respectively;

on lines 050, 080 of subsection 1.1 of section 1 - the amount of 6,000 rubles. and 54,000 rub. respectively.

3. The quarterly advance payment for 9 months will be:

600,000 rub. x 20% = 120,000 rub.

Thus, based on the tax base determined on an accrual basis from the beginning of the year to the end of 9 months, the organization will have an obligation to pay a quarterly advance payment.

The overpayment incurred by the organization at the end of the six months (60,000 rubles) was not offset against the payment of other taxes and was not returned to the organization’s current account. The amount of the overpayment is counted towards the payment of the quarterly advance payment based on the results of 9 months (paragraph 5, clause 1, article 287, clause 14, article 78 of the Tax Code of the Russian Federation). In this case, the amount payable to the budget at the end of 9 months will be 60,000 rubles. (120,000 rubles - 60,000 rubles).

In the tax return for 9 months, the quarterly advance payment will be reflected as follows:

on line 180 of sheet 02, enter the amount of 120,000 rubles;

on lines 190, 200 of sheet 02 - the amount is 12,000 rubles. and 108,000 rub. respectively;

on lines 210, 220 and 230 of sheet 02 - amounts 60,000 rubles, 6,000 rubles. and 54,000 rub. respectively;

on lines 270 and 271 of sheet 02 - the amount of 6,000 rubles. and 54,000 rub. respectively;

on lines 040 and 070 of subsection 1.1 of section 1 - the amounts are 6,000 and 54,000 rubles. respectively.

Procedure for calculating monthly advance payments

In accordance with paragraphs 3-5 of paragraph 2 of Art. 286 of the Tax Code of the Russian Federation, the monthly advance payment payable during each quarter of the current tax period is determined not from the actually received, but from the estimated profit, the amount of which is calculated based on the results of the previous quarter.Monthly advance payments should be calculated as follows:

1) the monthly advance payment paid in the first quarter of the current tax period (paragraph 3 of paragraph 2 of Article 286 of the Tax Code of the Russian Federation) is determined by the formula,

A1 = A4 of the previous tax period,

where A1 is the monthly advance payment due in the first quarter of the current tax period;

A4 of the previous tax period - monthly advance payment due in the fourth quarter of the previous tax period;

2) the monthly advance payment paid in the second quarter of the current tax period (paragraph 3 of clause 2 of article 286 of the Tax Code of the Russian Federation) is equal to:

A2 = AK1 / 3,

where A2 is the monthly advance payment due in the second quarter of the current tax period;

AK1 - quarterly advance payment calculated based on the results of the first quarter of the current tax period;

3) the monthly advance payment paid in the third quarter of the current tax period (paragraph 4 of paragraph 2 of Article 286 of the Tax Code of the Russian Federation) is calculated using the formula:

A3 = (AK2 - AK1) / 3,

where A3 is the monthly advance payment due in the third quarter of the current tax period;

AK2 - quarterly advance payment, calculated based on the results of the six months of the current tax period;

4) the monthly advance payment paid in the fourth quarter of the current tax period (paragraph 5 of paragraph 2 of Article 286 of the Tax Code of the Russian Federation) is equal to:

A4 = (AK3 - AK2) / 3,

where A4 is the monthly advance payment due in the fourth quarter of the current tax period;

AK3 is a quarterly advance payment calculated based on the results of nine months of the current tax period.

It should be noted that if during the current quarter an organization makes less profit than in the previous quarter, or even a loss, this does not exempt it from paying monthly advance payments in the current quarter. In such situations, the amount of monthly advance payments paid in the current quarter (or part thereof) will be recognized as an overpayment of income tax, which is subject to offset against future payments or a refund.

In the tax return based on the results of the tax period, monthly advance payments for the first quarter of the current year are not calculated. This is explained by the fact that such payments are equal to monthly advance payments calculated for the fourth quarter of the previous tax period, which in turn are reflected in the declaration for nine months.

The amount of monthly advance payments is reflected on line 290 of sheet 02, including lines 300 and 310, as well as lines 120-140, 220-240 of subsection 1.2 of section 1 of the tax return.

In accordance with paragraph 3 of paragraph 1 of Art. 287 of the Tax Code of the Russian Federation, monthly advance payments due during the reporting period are paid no later than the 28th day of each month of this reporting period.

EXAMPLE 3

Quarterly advance payments calculated based on the results of the reporting periods of the previous year for the Cascade organization amounted to:

for the six months - 700,000 rubles, including to the federal budget - 70,000 rubles, to the budget of a constituent entity of the Russian Federation - 630,000 rubles;

for 9 months - 1,300,000 rubles, including to the federal budget - 130,000 rubles, to the budget of a constituent entity of the Russian Federation - 1,170,000 rubles.

In the current year, advance payments based on the results of the reporting periods were equal to:

for the first quarter - 100,000 rubles, including to the federal budget - 10,000 rubles, to the budget of a constituent entity of the Russian Federation - 90,000 rubles;

a loss was incurred for the half-year, as a result of which the advance payment at the end of the half-year was equal to zero;

for 9 months - 200,000 rubles, including to the federal budget - 20,000 rubles, to the budget of a constituent entity of the Russian Federation - 180,000 rubles.

Let's determine the amount of the monthly advance payment that should be paid in each quarter of the current tax period and the first quarter of the next year.

1. The monthly advance payment payable in the first quarter of the current year is equal to the monthly advance payment that was paid by the organization in the fourth quarter of the previous year. Its calculation is carried out in the following order:

(1,300,000 rub. - 700,000 rub.) / 3 = 200,000 rub.

Thus, in January, February and March, the organization pays 200,000 rubles to the budget.

Since at the end of the first quarter the actual amount of the advance payment, determined based on the tax rate and the tax base calculated on an accrual basis, amounted to 100,000 rubles, the organization incurred an overpayment of tax in the amount of 500,000 rubles. (200,000 rub. x 3 - 100,000 rub.).

2. The monthly advance payment due in the second quarter of the current year is equal to:

100,000 rub. / 3 = 33,333 rub.

The organization calculated the monthly advance payments calculated for the second quarter in the tax return for the first quarter.

Due to the presence of an overpayment based on the results of the first quarter (RUB 500,000), the organization offset the overpaid amount against monthly advance payments for the second quarter.

Thus, the overpayment at the end of the second quarter amounted to 400,000 rubles. (500,000 rubles - 33,333 rubles x 3).

3. The organization did not pay monthly advance payments in the third quarter (July, August, September), since the difference between the quarterly and advance payments for the six months and the first quarter of the current year was negative (0 - 100,000 rubles = -100,000 rubles)

4. Quarterly advance payment for 9 months in the amount of 200,000 rubles. The organization credited the overpayment.

5. Monthly advance payments payable in the fourth quarter of the current year and the first quarter of the next year amounted to:

(200,000 rub. - 0 rub.) / 3 = 66,666 rub.

Thus, in October, November and December of the current year and in January, February, March of the next year, the amount of monthly advance payments was 66,666 rubles, including to the federal budget - 6,666 rubles each, to the budget of a constituent entity of the Russian Federation - 60,000 each rub. Since the organization has overpaid taxes, monthly advance payments can be offset.

Monthly advance payments based on actual profit received

In accordance with paragraph 2 of Art. 285 of the Tax Code of the Russian Federation, in the event of a transition to the procedure for paying monthly advance payments based on the actual profit received, the reporting periods will be recognized as one month, two months, three months, etc. until the end of the calendar year.The amount of the advance payment for the reporting period, paid based on the actual profit received, is calculated as follows:

AM reporting = NB x C,

where reporting AM is the amount of the advance payment calculated based on the results of the reporting period;

NB - tax base for the reporting period, calculated on an accrual basis from the beginning of the year to the end of the reporting period;

C is the tax rate.

The amount of the advance payment that must be paid to the budget based on the results of the corresponding reporting period is calculated according to the formula (paragraph 8, paragraph 2, article 286, paragraph 5, paragraph 1, article 287 of the Tax Code of the Russian Federation):

AM for additional payment = AM reporting - AM previous,

where AM for additional payment is the amount of the advance payment for the reporting period, subject to payment (addition) to the budget;

AM previous - the amount of the advance payment paid based on the results of the previous reporting period (in the current tax period).

The amount of the advance payment for the reporting period is determined based on the tax rate and the actual profit received in the reporting period, which is calculated on an accrual basis from the beginning of the tax period until the end of the corresponding month (paragraph 7, clause 2, article 286 of the Tax Code of the Russian Federation). At the same time, the difference between the amount of the advance payment accrued on an accrual basis from the beginning of the year and the advance payment accrued for the previous reporting period is transferred to the budget on a monthly basis.

Monthly advance payments for income tax are calculated in the manner established by clause 2 of Art. 286 Tax Code of the Russian Federation. Let's look at the general algorithm and give an example of calculating an advance payment for a month, and also talk about the features of using this procedure in some non-standard situations.

Algorithm for determining the amount of monthly advance payment

On a quarterly basis, the taxpayer calculates the amount of the advance on profits based on data obtained from the actual results of work for the period from the beginning of the year. However, at the same time (if he does not use the right to pay advances only quarterly), he must make payments ahead of this calculation, made monthly on time.

To determine the amount of such payments, clause 2 of Art. 286 of the Tax Code of the Russian Federation establishes the following dependencies:

- the monthly advance payment in the first quarter of the current year is equal to the monthly advance payment in the fourth quarter of the previous year;

- the monthly advance payment paid in the second quarter is equal to 1/3 of the quarterly advance payment for the first quarter of the current year;

- the monthly advance payment paid in the third quarter is equal to 1/3 of the difference between the advance payment for the six months and the advance payment for the first quarter;

- The monthly advance payment paid in the fourth quarter is equal to 1/3 of the difference between the advance payment for 9 months and the advance payment for six months.

Trade tax payers can reduce advance payments of income tax by the amount of trade tax actually paid in relation to the consolidated budget of a constituent entity of the Russian Federation (clause 10 of Article 286 of the Tax Code of the Russian Federation).

Read about where and for whom the trade tax applies in this material. .

What happens to the advance if there is a loss in the quarter?

In one quarter of the tax period, a taxpayer may receive less profit than in the previous one, or a loss. But these circumstances do not exempt the taxpayer from paying monthly advance payments in the current quarter. In such cases, the amount or part of the monthly advance payments paid in the current quarter will be recognized as an overpayment of income tax, which, according to clause 14 of Art. 78 of the Tax Code of the Russian Federation is subject to offset against upcoming payments for income tax or other taxes; for repayment of arrears, payment of penalties or refund to the taxpayer.

If the calculated amount of the monthly advance payment turns out to be negative or equal to 0, then monthly advance payments in the corresponding quarter are not paid (paragraph 6, paragraph 2, article 286 of the Tax Code of the Russian Federation). A similar result obtained based on the results of the third quarter leads to the absence of payment of advances in the fourth quarter of the current year and the first quarter of the next.

Calculation of advance payments during reorganization and when changing the payment procedure

In the event of a reorganization of a taxpayer, during which another legal entity is merged with it, the amount of the monthly advance payment on the date of reorganization is calculated without taking into account the performance indicators of the merging organization (letter of the Ministry of Finance of Russia dated July 28, 2008 No. 03-03-06/1/431).

If a taxpayer changes the procedure for calculating advances, moving from monthly determination of them from actual profit to monthly payments calculated quarterly, then this can only be done from the beginning of the new year (paragraph 8, paragraph 2, article 286 of the Tax Code of the Russian Federation), notifying the Federal Tax Service no later than 31 December of the year preceding the change. The amount of the monthly payment that will have to be paid in the first quarter, in this case, will be determined as 1/3 of the difference between the amount of the advance calculated based on the results of 9 months and the amount of the advance payment received based on the results of the half-year in the previous year (paragraph 10 p. 2 Article 286 of the Tax Code of the Russian Federation).

To learn about the timing of advance payments, read the article “What is the procedure and deadlines for paying income tax (postings)?” .

Example of calculating advance payments

Quarterly advance payments calculated based on the results of the reporting periods of the previous year for the Kvant organization amounted to:

- for half a year - 700,000 rubles;

- for 9 months - 1,000,000 rubles.

In the current year, advance payments based on the results of reporting periods (quarterly) amounted to:

- for the first quarter - 90,000 rubles;

- a loss was incurred for the half-year, as a result of which the advance payment at the end of the half-year was equal to zero;

- for 9 months - 150,000 rubles.

It is necessary to determine the amount of the monthly advance payment that the Kvant organization should pay in each quarter of the current tax period and the first quarter of the next year.

Solution

1. The monthly advance payment payable in the first quarter of the current year is equal to the monthly advance payment that was paid by the Kvant organization in the fourth quarter of the previous year (paragraph 3, paragraph 2, article 286 of the Tax Code of the Russian Federation). Its calculation is carried out in the following order:

(1,000,000 rub. - 700,000 rub.) / 3 = 100,000 rub.

Consequently, in January, February and March, the Kvant organization pays 100,000 rubles each. advances, distributing them among budgets in the required proportion.

Since at the end of the first quarter the actual amount of the advance payment, determined based on the tax rate and the tax base calculated on an accrual basis, amounted to 90,000 rubles, the organization incurred an overpayment of tax in the amount of 210,000 rubles. (RUB 100,000 × 3 - RUB 90,000).

2. Monthly advance payment due in the second quarter of the current year: RUB 90,000. / 3 = 30,000 rub.

The Kvant organization calculated monthly advance payments calculated for the second quarter in the tax return for the first quarter.

Due to the presence of an overpayment based on the results of the first quarter (RUB 210,000), the overpaid amount was offset against the monthly advance payments for the second quarter.

Thus, the overpayment at the end of the second quarter amounted to 120,000 rubles. (RUB 210,000 - RUB 30,000 × 3).

3. The Kvant organization did not pay monthly advance payments in the third quarter (July, August, September), since the difference between the quarterly advance payment for the half-year and the quarterly advance payment for the first quarter of the current year was negative (0 - 90,000 rubles = - 90,000 rubles) (paragraph 6, clause 2, article 286 of the Tax Code of the Russian Federation).

4. Quarterly advance payment for 9 months in the amount of 60,000 rubles. credited towards the overpayment.

5. Monthly advance payment due in the fourth quarter of the current year and the first quarter of the next year:

(150,000 rub. - 0 rub.) / 3 = 50,000 rub.

Thus, in October, November and December of the current year, as well as in January, February and March of the next year, the amount of monthly advance payments will be 50,000 rubles. Since the Kvant organization has overpaid taxes, monthly advance payments can be offset.

Results

The rules for determining the amount of monthly advances paid on profit are established by the Tax Code of the Russian Federation and are described in relation to each quarter. This value is determined for each subsequent quarter by the amount of actually calculated tax attributable to the previous quarter. The monthly advance is taken from this amount as 1/3. Receiving a loss at the end of a quarter eliminates the need for advance payments in the following quarter.

All commercial organizations in Russia pay income tax in installments throughout the year. The tax service requires advance payments - intra-annual and annual payments, as well as monthly advance payments for income tax are included in this list. Today we will talk about how to calculate them correctly and who should pay.

Obligations to pay income tax are assigned to the following organizations:

- OJSC, CJSC, LLC, i.e. all Russian legal entities.

- Foreign organizations that have actual management in the country.

- Foreign companies recognized as tax residents of the Russian Federation.

- Legal entities that are foreigners but receive income from Russian sources.

- Permanent representative offices of foreign companies in the country.

The following are exempt from paying tax:

- organizations that do not have taxable objects;

- enterprises applying a specialized tax regime;

- companies participating in the Skolkovo innovation center.

Monthly advance payments for income tax: how much to pay?

The income tax rate is most often 20%. The amount of tax paid by commercial firms is divided between the regional and federal budgets. However, only 3% goes to the state. The remaining 17% goes to regional budgets.

Some regions practice lowering rates for certain groups of commercial organizations. For “special” taxpayers, up to 13.5% tax is established.

The rate may be even lower, but only for the following companies:

- enterprises recognized as residents in the territory of the Vladivostok port or in areas of rapid economic development;

- companies participating in investment projects at the regional level;

- partners in free or special economic zones.

Payment options

Only some companies are given the opportunity to pay taxes not monthly, but less often - every quarter. The following are entitled to relief:

- representative offices of foreign companies constantly conducting commercial activities on the territory of the Russian Federation;

- budgetary organizations (exceptions - museum, theater, library);

- companies with small profits - no more than 15 million for each of the four previous quarters;

- autonomous institutions;

- organizations conducting non-profit activities.

Other companies must remit tax every month. The law provides two payment options:

- Deposit funds monthly and pay the balance quarterly.

- Calculate the amount of monthly advances based on the profit received by the organization in the previous month.

Contributions based on profits earned in the previous month

This option is available to absolutely all organizations without exception. The tax amount is calculated from the revenue that the company received during the reporting period (one, two, three or more months).

To start using this tax payment regime from the upcoming calendar year, fill out an application and submit it to the nearest branch. The transition must be made no later than December 31st. For example, if in 2018 the management of an enterprise plans to make monthly payments, which should be calculated from the actual profit received, an application to the tax authority must be submitted by December 31, 2017.

On a note! After submitting and accepting an application to the Federal Tax Service, you need to start monthly income tax calculations in January. Further transfers must be made on the 28th of the month following the reporting month. The January transfer of money to the budget must be made before February 28, the February transfer - before March 28. March - until April 28.

How to calculate advance payments for company income tax?

The amount that the company is obliged to pay to the state is calculated using the formula:

Payment amount = tax base for the reporting period of time (calculated on an increasing basis) * tax rate - the amount of payments that have already been paid previously for the reporting period of time

Example. In 2016, Snezhinka LLC calculated payments based on revenue received in previous quarters. That year, Snezhinka received income:

- in the first quarter - 20 million rubles;

- in the second - 10 million rubles;

- in the third - 15.5 million rubles;

- in the fourth - 24.5 million rubles.

Business income for the year amounted to 70 million rubles. On average, “Snowflake” earned 17.5 million for each quarter of the year we were looking at. This exceeds the government's cap of 15 million for each quarter.

In December 2016, Snezhinka was forced to switch to a tax calculation system based on profits received in the previous month.

Snezhinka’s profit for January 2017 was 120,000 rubles. Until February 28, 2017, the company must transfer 24,000 rubles (120,000 * 20%) to the budget.

In February, the company earned 80,000 rubles. The advance payment should be calculated as follows:

(120,000 +80,000) * 20% - 24,000 = 16,000 rubles

On a note! If at the end of the reporting period you received a loss, the amount of the advance that the company owes in the current period will be less than the amount of the advance paid for the previous period. In this case, the commercial organization does not owe anything.

Example. In January 2017, Vector LLC made a profit of 1 million rubles and paid an advance payment for this period in February. The contribution amount is 200 thousand rubles (1,000,000*20%). In January and February, Vector suffered losses amounting to 500 thousand rubles. There is no need to pay an advance payment for this period, since there was no profit. In this case, the previously paid 200 thousand rubles are considered overpaid. The overpayment will go towards paying the next periods of income tax or other tax. If the amount of the advance payment for January-March does not cover the overpayment, i.e. will be less than 200 thousand rubles, the balance will be transferred to the next reporting period.

Advances with additional payment per quarter

This method of calculating an advance payment is used by organizations that:

- do not have the right to deduct tax once a quarter;

- did not independently switch to calculating the advance on actually earned profits.

On a note! The advance must be calculated from the beginning of the year on an accrual basis.

The amount of the first quarterly contribution is equal to the amount of the contribution for the last three months of the previous year. So, the January, February and March advance payment is equal to:

1/3 * profit earned for the entire fourth quarter * effective tax rate

The amount of the contribution for the next quarter is equal to the amount of the first quarterly advance. In April, May and June the same amount should be received as in March, February and January of the same year.

The amount of contributions in the third reporting quarter = the amount of contributions for the first six months - the amount of the first quarterly advance.

In July, August and September the budget should receive:

1/3 * (profit earned in six months - amount already paid for the previous 6 months)

The amount of contributions in the fourth quarter = the amount of contributions for a nine-month period - the amount of advances paid in the first half of the year.

The October, November and December monthly advance payment is equal to one third of the difference in profit for the period from January to September and the previously paid tax amount.

On a note! At the end of each quarter, the organization's accountant compares the total amount of monthly advance payments and the actual profit received. If the amount of contributions is less than the tax, the balance must be paid. The deadline for transferring money is the 28th of the month following the reporting quarter.

Example. In 2016-2017, Udacha LLC paid advance payments every 30 days, paying extra for each quarter.

Table 1. Organizational profit

First quarter advance = 1/3 * 1,200,000 * 20% = 96,000 rubles

So, January, February and March transfers should be 96,000 rubles. The amount of the surcharge based on the results of the first quarterly period will be calculated as follows:

11,000,000 * 20% – 96,000 * 3 = 12,000 rubles. Additional payment must be made by April 28. This means that in April the organization must pay a contribution for March and an additional payment for the quarter of 12,000 + 96,000 = 108,000 rubles.

Monthly advances in the second quarter are equal to a third of profits in the first quarter.

1,100,000 * 20% * 1/3 = 80,667 rubles

In April, March and June, the budget should receive 80,667 rubles each.

For six months, the profit of “Luck” amounted to 2,000,000 (1,100,000 + 900,000). For the first 6 months you will receive an overpayment:

2 000 000 * 20% – (96 000 * 3) – 12 000 – (80 667 * 3) = — 142 000

The company can return this amount back or keep it towards future payments. “Luck” chose the first option.

Advances in the third quarter:

(2,000,000 * 20% - 900,000 * 20%) / 3 = 73,333 rubles.

This amount must be paid in July, August and September.

Tax for new organizations

Organizations that have been created recently pay taxes a little differently. New companies can choose one of two methods for paying upfront fees:

- Calculation of advance payments based on quarterly results. All organizations use this option “by default”, so there is no need to notify the tax service about the transition to the system. A company established in December makes contributions based on the profits earned during the period from December to March. The deadline for payment is April 28 of the current year. The organization begins to apply the general procedure for transferring contributions in the sixth quarter. The company, founded in June, is moving to a single system for all organizations in the third quarter of next year.

- Calculation of advance payment based on actual profit. If company management decides to use this tax payment option, the tax office must be notified. A company created in December begins to pay monthly advances, which the accountant calculates from the profits received in December-January. The deadline for transferring funds is February 28.

Deadlines

The company must make a payment every month during the calendar year. But the period January-December is not considered reporting; there is no requirement to pay an advance for this time at the beginning of the next year.

The calendar year January-December is recognized as a tax period, so tax money must be sent no later than March 28 of the year following the reporting year.

Example. In 2017, Avtotransport LLC paid every month from February to December. The total amount was 100,000 rubles. At the end of the year, the company must pay 120,000 rubles, i.e. 20,000 rubles remained unpaid at the beginning of the new year 2018. They must be submitted by March 28, 2018.

How are taxes calculated?

To correctly calculate how much tax you need to pay, you need to know which expenses and income should be included in the report, and which do not need to be indicated. The law allows two methods for determining the dates when these transactions can be recognized.

First method. Accrual

The time of actual receipt of funds or incurrence of costs does not play any role. Income and expenses are recognized when they are reflected in the documents. If the income of funds and expenses have an indirect relationship that cannot be clearly determined, the company itself distributes income using the principle of uniformity. The date of sale of finished goods (provision of services) is considered the date of the transaction. It doesn’t matter when exactly the money arrived.

The date of receipt of non-operating revenue is recognized as follows:

- for dividends - the date when the money arrived in the recipient's current account;

- for donated property or other similar income - the date of signing the acceptance and transfer document.

Second method. Cash

The cash method is the exact opposite of the accrual method. The date of receipt of profitability is the date of receipt of money at the cash desk or in the current account of the enterprise, receipt of property rights, etc. Costs are recognized only after they are paid, that is, when the money leaves the cash register.

On a note! Only companies whose average quarterly profitability for the previous year reached a maximum of 1 million rubles have the right to use the cash method.

What is considered income?

Profit is the difference between cash (or property) inflows and business expenses. Income includes not only income from sales, but also any other earnings of the company. For example, interest on deposits in financial institutions or profit from renting out real estate. When taxing, value added tax and excise taxes are deducted from income.

Amounts received by the organization are confirmed by:

- tax accounting documents;

- primary documents;

- other documents confirming receipt of money.

Companies do not pay taxes on all proceeds. The law defines several types of income that are exempt from taxation:

- contributions to the company's management company;

- property acquired in the form of collateral or deposit;

- property issued on credit;

- an object of possession received free of charge.

The organization must take into account all other proceeds when calculating tax.

What expenses to record?

Expenses are expenses of a business. They need to be justified and confirmed with documents. Expenses are divided into two groups:

- Expenses for the sale or production of goods and services- personnel wages, depreciation, purchase of primary raw materials and other material costs.

- Non-operating expenses- legal costs, loss due to negative exchange rates, etc.

On a note! Taxation does not take into account expenses for loan repayment, transfers to the organization's management company, dividend payments, etc.

Selling costs can be direct or indirect. The first category includes the enterprise’s costs for labor, material costs, and depreciation. Each month, direct costs are distributed by the enterprise and included in the cost of the final product or work in progress. This type of expense reduces the tax base strictly as the goods (services) are sold, in the price of which they are taken into account. What exactly is included in the list of direct expenses is decided by the taxpayer himself, in accordance with his accounting policies.

Indirect costs are costs that are neither direct nor non-operating. They cannot be part of the cost of the final product (service provision). Indirect costs include rent, utilities and other expenses associated with the operation of the company. When calculating income tax, this type of expense must be included in the expenses of the current reporting period.

What to do in case of overpayment?

If there was a mistake and you overpaid more tax than necessary, you can get your money back. The taxpayer has 3 years from the date of filing the tax return rather than paying the advance. If tax officials do not agree to return the money, insist. The law is on your side.

How do enterprises that are deprived of the right to use the simplified taxation system pay income tax?

If a company's income exceeds the limit established by the state, the commercial enterprise is deprived of the right to a simplified tax payment regime. The first time after losing the simplified tax system, the company must make tax payments as a new organization, that is, transfer advance payments every 30 days, starting from the end of the entire quarter. The date of formation of the company will be considered the date when it made the transition to the standard tax system.

If an organization switched to the regular system from the beginning of October 2016, it must begin making contributions after the end of the fourth quarter of 2016. Advances must go to the budget starting in January 2017. But, according to the law, the amount of advances for the first quarter is equal to the amount of advances for the fourth quarter. Since there are no contributions for that period, the company has no way to calculate the payment amount. Therefore, the obligation to transfer payments arises for our organization only in the second quarter of 2017.

Filing declarations

Income tax reporting is submitted

- For a month - before the 28th day of the month following the reporting month.

- For a year - before March 28 of the year following the tax period.

The completed declaration must be submitted to the tax authority located at the location of the company. A separate division of a large company submits the document to the branch, which is located at the location of this branch.

Penalties for non-payment of tax

If an organization does not transfer tax money within the prescribed period, it faces penalties. The tax office has the right to collect the required amount from the debtor at the expense of the property or withdraw it from the bank account.

Within three months after the delay is discovered, the company is sent a demand for payment of income tax. This document indicates the repayment period and amount of the debt.

On a note! The decision to collect the tax debt is made a maximum of 2 months after the payment deadline has expired.

If you transfer an advance payment for a smaller amount than indicated in the declaration, the tax office has the right to forcibly collect the difference. Transferring an insufficient amount may result in a penalty. But, if the initially declared amount exceeds the actual profit, the amount of the penalty may be recalculated.

For some reason you forgot to submit your return on time? In ours you can familiarize yourself with the list of tax sanctions, and we will also consider options for reducing the amount of the fine.

How to save on tax legally?

The tax office is improving its control over companies, so saving on taxes is becoming increasingly difficult. But there are legal ways to reduce your premiums.

To save money, you can recognize revenue from payments. If a product is sold, but payment for it has not been received, the supplier is considered the owner of the product. The enterprise's income must include revenue on the date of actual payment.

Another way to reduce your current premiums is to create a reconciliation statement with the lender. This will help delay paying off old debts. This way you can defer the inclusion of the loan in your income for 3 years.

One method to save on premiums is to offset mortgage interest. But it needs to be formatted correctly. If it is not included in wages, then insurance may not be paid for. Because funds to pay off interest on the purchase of residential real estate, which the company provides to employees, are not subject to contributions.

Video - Advance payments for income tax

Today we will consider the topic: “calculation of advance payments for property tax” and will analyze it based on examples. You can ask all questions in the comments to the article.

Calculation of the amount of advance payments for property tax

What determines the need to submit a calculation of advances on property

Rules for calculating and paying property tax for legal entities, described in Chapter. 30 of the Tax Code of the Russian Federation, largely depend on the provisions of the legislation of the constituent entity of the Russian Federation in which the objects subject to this tax are located. The subject has the right to independently establish (clause 2 of Article 372 of the Tax Code of the Russian Federation):

- additional (in comparison with Article 381 of the Tax Code of the Russian Federation) benefits and rules for their application;

- the procedure for calculating the tax base for individual real estate objects;

- the amount of the rate (without going beyond its upper limits indicated in Article 380 of the Tax Code of the Russian Federation);

- the procedure for making tax payments (including the availability of advances for it);

- deadlines for paying both tax and advances (if they are introduced in the region).

Thus, the rules for calculating and paying tax by region may vary significantly. Therefore, before you start calculating advance payments for property taxes, you should find out whether they have been introduced in the region. Such a decision in a legislative document of a constituent entity of the Russian Federation will be equivalent to an indication that reporting periods for taxes have not been established. This allows you to use clause 3 of Art. 379 Tax Code of the Russian Federation. The absence of a reporting period entails the right of the taxpayer:

- do not pay advances during the year;

- do not submit calculations on them.

Moreover, the region has the right to make such a decision not in relation to all taxpayers, but only for certain categories of them (clause 6 of Article 382 of the Tax Code of the Russian Federation).

If there is no decision not to establish reporting periods in the region, then the obligation to submit settlements for advances and pay them is not removed from the taxpayer.

Time limits established for advances on property

The deadline for paying advances by constituent entities of the Russian Federation will also vary (clause 1 of Article 383 of the Tax Code of the Russian Federation). Meanwhile, the deadline for submitting calculations for them is established as a single one - no later than 30 calendar days from the end of the period corresponding to the reporting period (clause 2 of Article 386 of the Tax Code of the Russian Federation).

- quarter, half-year, 9 months, if the base is determined by the average (average annual) cost;

- quarter, if the base depends on the cadastral valuation.

Considering the coincidence of the end of the reporting periods for both bases, reporting on advances regarding the property of legal entities will have to be submitted no later than the 30th of months such as April, July, October. If this date coincides with a general day off, the deadline will be transferred to the weekday following this weekend (Clause 7, Article 6.1 of the Tax Code of the Russian Federation).

Payments for advance payments are submitted to the tax authority corresponding to the location of the taxable object (clause 1 of Article 386 of the Tax Code of the Russian Federation). There are only two exceptions to this rule:

- the largest taxpayers only need to submit a report at their place of registration as the largest;

- for property located in the seas or on the shelf within the Russian Federation, in the economic zone of the Russian Federation of exclusive significance or outside the Russian Federation (for Russian legal entities), the calculation is submitted at the place of registration of the legal entity or representative office of a foreign company that has objects subject to taxation in the Russian Federation.

Moreover, in the second case, if the property is used for study, exploration, preparation for development or development of offshore hydrocarbon deposits, advances on it are not calculated.

For information about which tax inspectorate to submit reports to if the taxpayer’s address has changed, read the publication “Calculation of advance payments for property tax - where to submit when changing address?”

Differentiation of property for the purposes of calculating tax on it

When starting to calculate the amount of the advance payment for property tax, you need to keep in mind that the result of this process will have to be divided depending on (clauses 1, 2, article 376, clause 3, article 382 of the Tax Code of the Russian Federation):

- places where the property is located;

- types of taxable objects;

- tax rates established for these types;

- options for applicable benefits.

These circumstances will determine the need:

- creating reports intended for different Federal Tax Service Inspectors;

- categorization of property into different sections of the report;

- creating several sheets of the same section, including this may be required for the same object;

- summing up the calculation results relating to the same area to reflect the total accrual amounts.

The distribution into different sections is predetermined, first of all, by the base from which the tax is calculated. Such a base can be either the average (average annual) value (in the general case) or the cadastral value (for real estate of certain types or a certain affiliation).

How to calculate the tax base based on the average (average annual) cost

The concept of average cost is applicable only in relation to property available in the reporting period (clause 4 of article 376 of the Tax Code of the Russian Federation). For calculations over a year, it is called the annual average (annual average). But the principles for determining the average and annual average cost are the same. This calculation is made for all taxable objects as a whole, without singling out specific units from their list. Before its implementation, those that:

- is not considered an object for taxation (clause 4 of article 374 of the Tax Code of the Russian Federation);

- exempt from tax (Article 381 of the Tax Code of the Russian Federation);

- taxed on a different basis (Article 378.2 of the Tax Code of the Russian Federation);

- refers to capital investments in some objects made in the period from 01/01/2010 to 12/31/2024 (clause 6 of article 376 of the Tax Code of the Russian Federation).

This article will be useful to those taxpayers who make quarterly payments based on the results of the quarter plus monthly advance payments.

The article will help:

- calculate advance payments for income tax,

- find out about the timing of advance payments based on the results of the first quarter,

- fill out the appropriate sections and lines in the declaration for the first quarter.

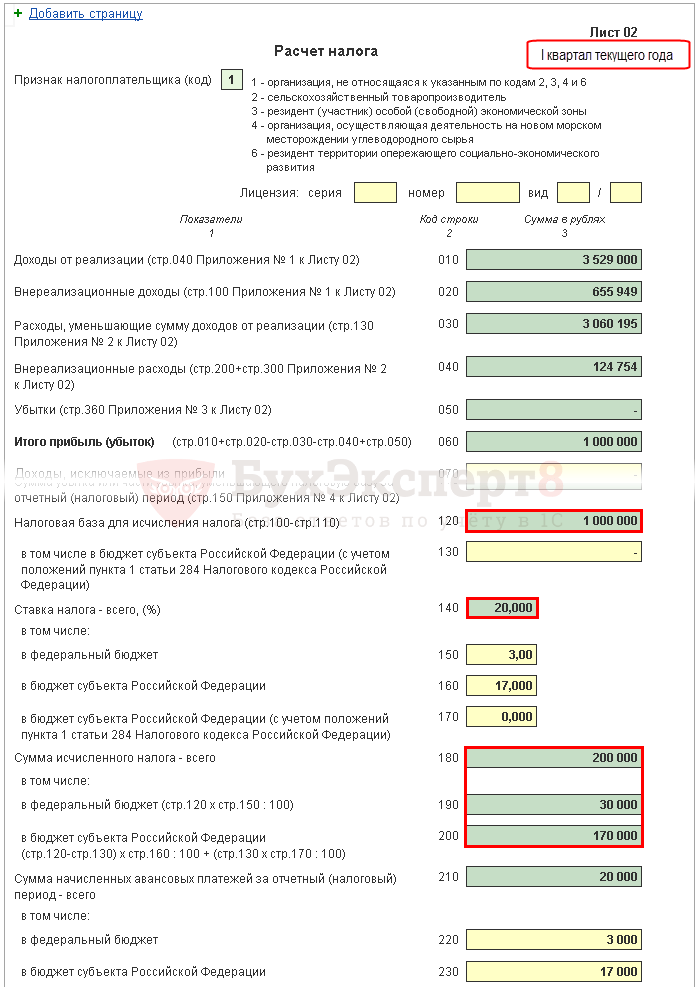

Example

Sheet 02 Calculation of income tax and advance payments

Let's look at the step-by-step filling out of the Sheet 02 declaration regarding the calculation of income tax for the first quarter and the amount of monthly advance payments for the second quarter.

Step 1. Determine the amount of income tax for the first quarter (pages 180-200)

The amount of income tax in 1C is calculated automatically based on the tax base indicated on page 120 and the rate on page 140 (150-170).

Check the calculation for the first quarter using the formula:

In our example, the total amount of income tax (page 180) is 1,000,000 x 20% = 200,000 rubles, including:

- to the federal budget (p. 190) - 1,000,000 x 3% = 30,000 rubles;

- to the budget of a constituent entity of the Russian Federation (page 200) - 1,000,000 x 17% = 170,000 rubles.

Step 2. Enter the amount of advance payments calculated for the previous period (pages 210-230)

Advance payments, which the organization must pay monthly in the first quarter, are calculated in the declaration for 9 months of the previous year. Therefore, in lines 220, 230, manually enter advance payments from lines 330, 340 of the declaration for 9 months.

The following equality must be satisfied:

In our example, in the declaration for 9 months of last year, the total amount of accrued advance payments (p. 320) is 20,000 rubles, including:

- federal budget (p. 330) - 3,000 rubles;

- budget of a constituent entity of the Russian Federation (p. 340) - 17,000 rubles.

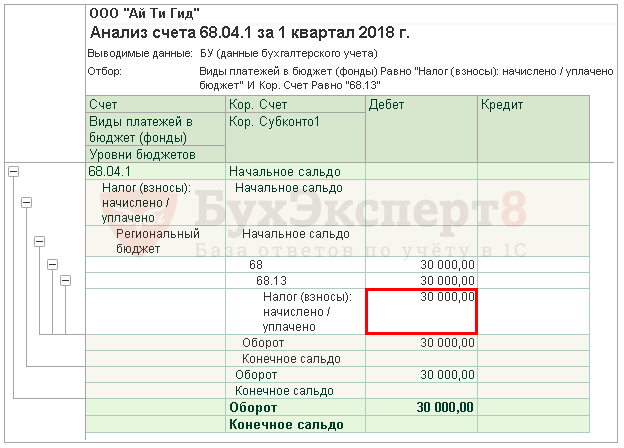

Step 3: Check the amount of trade fee paid (pages 265, 266, 267)

Lines 265, 266, 267 of Sheet 02 of the declaration will be filled out automatically in 1C if the organization has registered a retail outlet in the program and automatically calculates the trade fee.

In the declaration for the first quarter, these lines are filled in as follows:

- p. 265 – the amount of trade tax actually paid to the budget of a constituent entity of the Russian Federation since the beginning of the year. In our example, the amount is 30,000 rubles.

- page 266 - not filled out in the declaration for the first quarter, since the amount of the trade fee by which the tax was reduced in the previous quarters of the reporting year must be indicated.

- p. 267 – the amount of the trade fee, which reduces the calculated income tax for the first quarter to the republican budget. The line indicator cannot be greater than the amount on page 200 “Amount of accrued tax to the budget of a constituent entity of the Russian Federation.”

In 1C, line 267 automatically fills in the amount of the reduction in income tax on the trading fee for the first quarter, i.e. this is the turnover:

- Dt 68.04.1 ( Budget level - Regional budget, Payment type - Tax accrued/paid).

- Kt 68.13 ( Payment type - Tax accrued/paid).

In our example, page 267 is equal to 30,000 rubles.

Step 4. Determine the amount of tax to be paid additionally (pages 270, 271) or reduced (pages 280, 281)

Now it is necessary to determine which is greater: the amount of tax calculated based on the results of the first quarter (pp. 190, 200), or the amount of accrued advance payments that the taxpayer was obliged to pay in the first quarter (p. 220, 230) taking into account the trade tax ( p. 267).

Step 4.1. Federal budget

If page 190 is greater than page 220, then the tax to the federal budget based on the results of the first quarter must be paid additionally, i.e. in 1C line 270 will be automatically filled in according to the formula:

If page 190 is less than page 220, then the tax to the federal budget based on the results of the first quarter will be reduced, i.e. in 1C line 280 will be automatically filled in according to the formula:

In our example, line 190 (amount of 30,000 rubles) is greater than line 220 (amount of 3,000 rubles), therefore, the tax to the federal budget at the end of the first quarter will be additionally paid:

- page 270 = 30,000 - 3,000 = 27,000 rub.

Step 4.2. Budget of a constituent entity of the Russian Federation

If page 200 is greater than the sum (page 230 + page 267), then the tax to the budget of the constituent entity of the Russian Federation based on the results of the first quarter must be paid additionally, i.e. in 1C line 271 will be automatically filled in according to the formula:

If page 200 is less than the sum (page 230 + page 267), then the tax to the budget of the constituent entity of the Russian Federation based on the results of the first quarter will be reduced, i.e. in 1C line 281 will be automatically filled in according to the formula:

In our example, line 200 (amount 170,000 rubles) is greater than the sum of lines 230 and 267 (47,000 = 17,000 + 30,000), therefore, the amount of tax to the budget of a constituent entity of the Russian Federation at the end of the first quarter will be additionally paid:

- page 271 = 170,000 - 17,000 - 30,000 = 123,000 rubles.

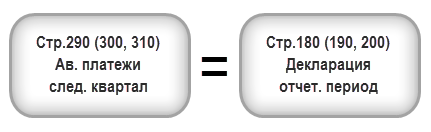

Step 5. Determine the amount of advance payments payable in the second quarter (pages 290-310)

Organizations paying monthly advance payments must, based on the results of the first quarter, calculate the advances payable in the second quarter. Such payments are reflected on line 290 (300, 310).

In 1C, these lines are filled in manually. Advance payments payable must be calculated using the formula:

In our example, the amount of monthly advance payments payable in the second quarter (line 290) is taken from line 180 (RUB 200,000), including:

- to the federal budget (p. 300) = p. 190 = 30,000 rubles;

- to the budget of a constituent entity of the Russian Federation (line 310) = line 200 = 170,000 rubles.

Section 1 Subsection 1.1 Final data on tax payment for the first quarter

Filling out the final data on additional payment or reduction of income tax in the first quarter is carried out in 1C automatically according to the following algorithm.

If the tax amount is due for additional payment, i.e. line 270 or line 271 is filled in in Sheet 02, then the amount indicated in them is transferred to Section 1 Subsection 1.1: PDF

- on page 040 - from page 270 of Sheet 02 “to the federal budget”;

- on page 070 - from page 271 of Sheet 02 “to the budget of a constituent entity of the Russian Federation.”

If the tax amount is reduced, i.e. line 280 or line 281 is filled in in Sheet 02, then the amount indicated in them is transferred to Section 1 Subsection 1.1: PDF

- on page 050 - from page 280 of Sheet 02 “to the federal budget”;

- on page 080 - from page 281 of Sheet 02 “to the budget of a constituent entity of the Russian Federation.”

In our example, the amount of income tax based on the results of the first quarter for the federal budget and the budget of a constituent entity of the Russian Federation was subject to additional payment.

Based on this norm, pay the tax for the first quarter specified in Section 1 of Subsection 1.1. necessary until April 28.

If the deadline for tax payment falls on a weekend or holiday, then the deadline is postponed to the first working day following it (Clause 7, Article 6.1 of the Tax Code of the Russian Federation).

Familiarize yourself with the procedure for paying income tax:

- federal budget;

- budget of a constituent entity of the Russian Federation.

In our example, additional payment of income tax must be made before April 30, 2018. (April 28 - day off):

- to the federal budget - 27,000 rubles.

- to a subject of the Russian Federation - 123,000 rubles.

Section 1 Subsection 1.2 Advance payments for the second quarter

In Section 1 Subsection 1.2. The declaration reflects monthly advance payments that must be paid in the second quarter.

The amount of advance payments for the second quarter was calculated on pages 300, 310 of Sheet 02. It is automatically distributed to Subsection 1.2 in the amount of 1/3 of the quarterly amount:

- pp. 120-140 - from page 300 “to the federal budget”;

- pp. 220-240 - from page 310 “to the budget of a constituent entity of the Russian Federation.”

Based on this norm, in the second quarter it is necessary to pay the advance payments specified in Section 1 of Subsection 1.2:

- until April 28;

- until May 28;

- until June 28.

If the deadline for payment of advance payments falls on a weekend or holiday, then the deadline is postponed to the first working day following it (Clause 7, Article 6.1 of the Tax Code of the Russian Federation).

- Payment of income tax to the federal budget;

- Payment of income tax to the budget of a constituent entity of the Russian Federation.

In our example, payment of advance payments in the second quarter should be made:

- until April 30, 2018 (April 28 - day off):

- to a subject of the Russian Federation - 56,666 rubles.

- until May 28, 2018:

- to the federal budget - 10,000 rubles.

- to a subject of the Russian Federation - 56,666 rubles.

- until June 28, 2018:

- to the federal budget - 10,000 rubles.

- to a subject of the Russian Federation - 56,668 rubles.